The Trickle-Down Effect of Too Much Debt

One would think we learned something from watching the US housing market collapse at the end of the previous decade. Yet, here we are, seven or so years later and many are making the same mistakes that were made by countless US homeowners.

Granted, the macro factors that helped to create the US housing crisis are not prevalent here in Canada. My favorite term from the US crisis was “NINJA” Mortgage: No Income? No Job? …APPROVED! Lending criteria in Canada isn’t quite that liberal.

What exacerbated the problem in the US was how homeowners were using their homes as a personal ABM, taking cash out whenever they wanted for whatever they wanted from the rapidly growing equity they had in their homes because the house values just kept increasing. They leveraged the “found” equity they had in their homes to feed their consumer appetite.

Here in Canada, and specifically farms on the Canadian Prairies, we’ve seen something similar. Rapidly appreciating farm land is being used to secure more borrowing, and often to secure the consolidation of other loans. The renaissance of farmland value appreciation, especially in Saskatchewan, added a dangerous amount of fuel to a fire of pent up demand. Land “equity” was used for the feverish acquisition of equipment, buildings, and more land.

In the US, while sub-prime mortgages kept payments low, everyone was happy to be ticking along with borrowing and spending to their heart’s content…until the sub-prime period ended and the piper needed to be paid. With a property fully leveraged and no ability to repay the debt, many homeowners resigned themselves to foreclosure. Those who may have had an ability to pay the debt saw the value of their fully leveraged property start to decline because of all the other foreclosures, so when they found themselves underwater, they too went the route of foreclosure.

No one is arguing that things are different here. True. Borrowing criteria is more stringent in Canada. What is similar, however, is the experience of a rapid appreciation in the value of real estate and the leverage of said appreciation to support more (other) debt.

I was talking with a 17,000ac farmer recently who was very aggressive in expansion over the last several years. He has increased the size and scale of his farm in every way: land, equipment, labor, and debt. He made no bones about continuing to leverage all assets, including the appreciating land and his depreciating equipment, to the fullest extent in an effort to facilitate further expansion. The scourge of his actions over these last few years was the incredible drain on his cash flow to service all this debt. This came to light for him when recently he needed land equity to source an operating line of credit so that he could meet his debt payments.

Direct Questions

Have most of the increases to equity on your balance sheet come from appreciation of asset values or have they come from building your retained earnings?

How has your Debt to Net Worth changed over the last few years?

Are you drawing on your operating line of credit to make loan payments?

From the Home Quarter

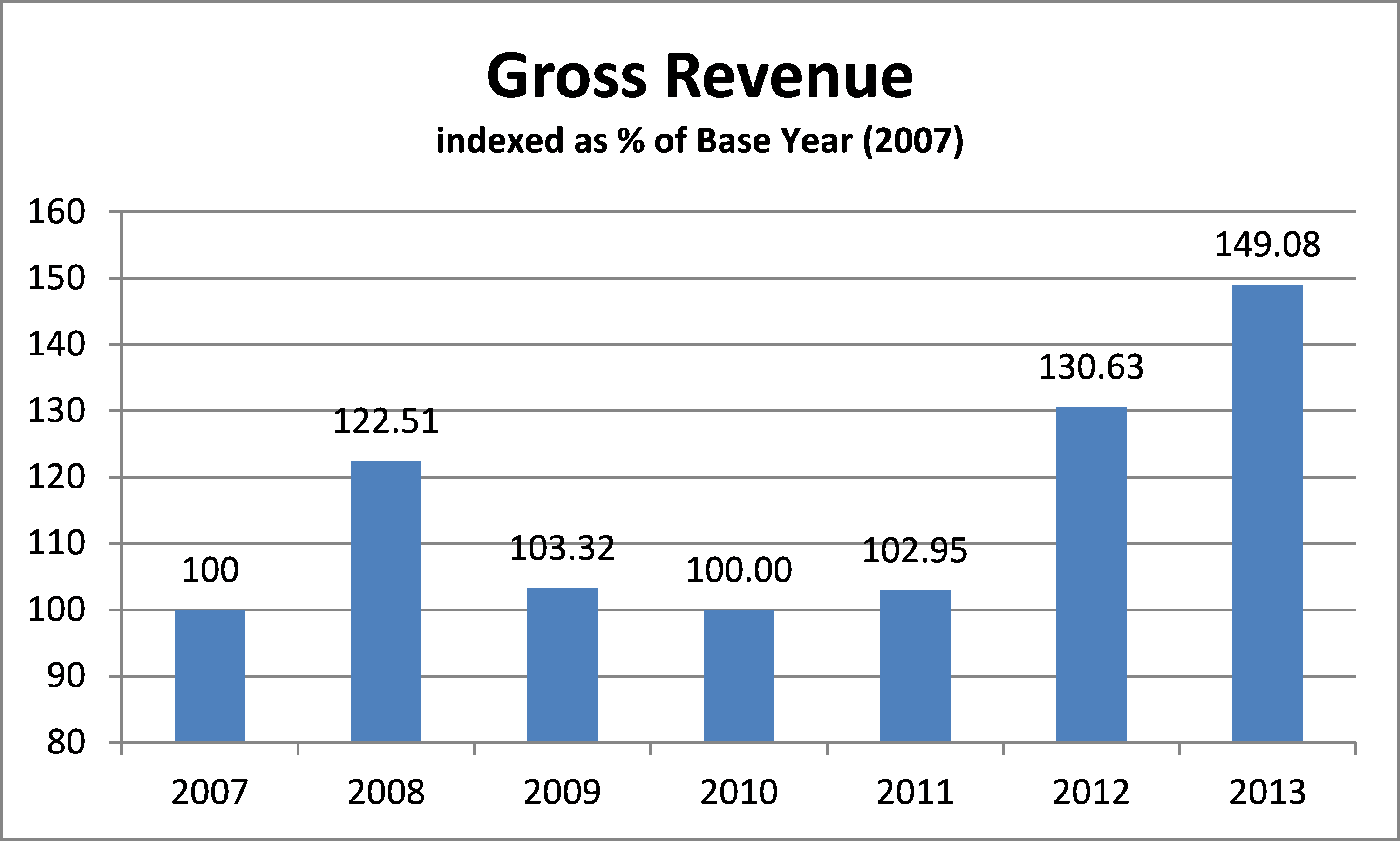

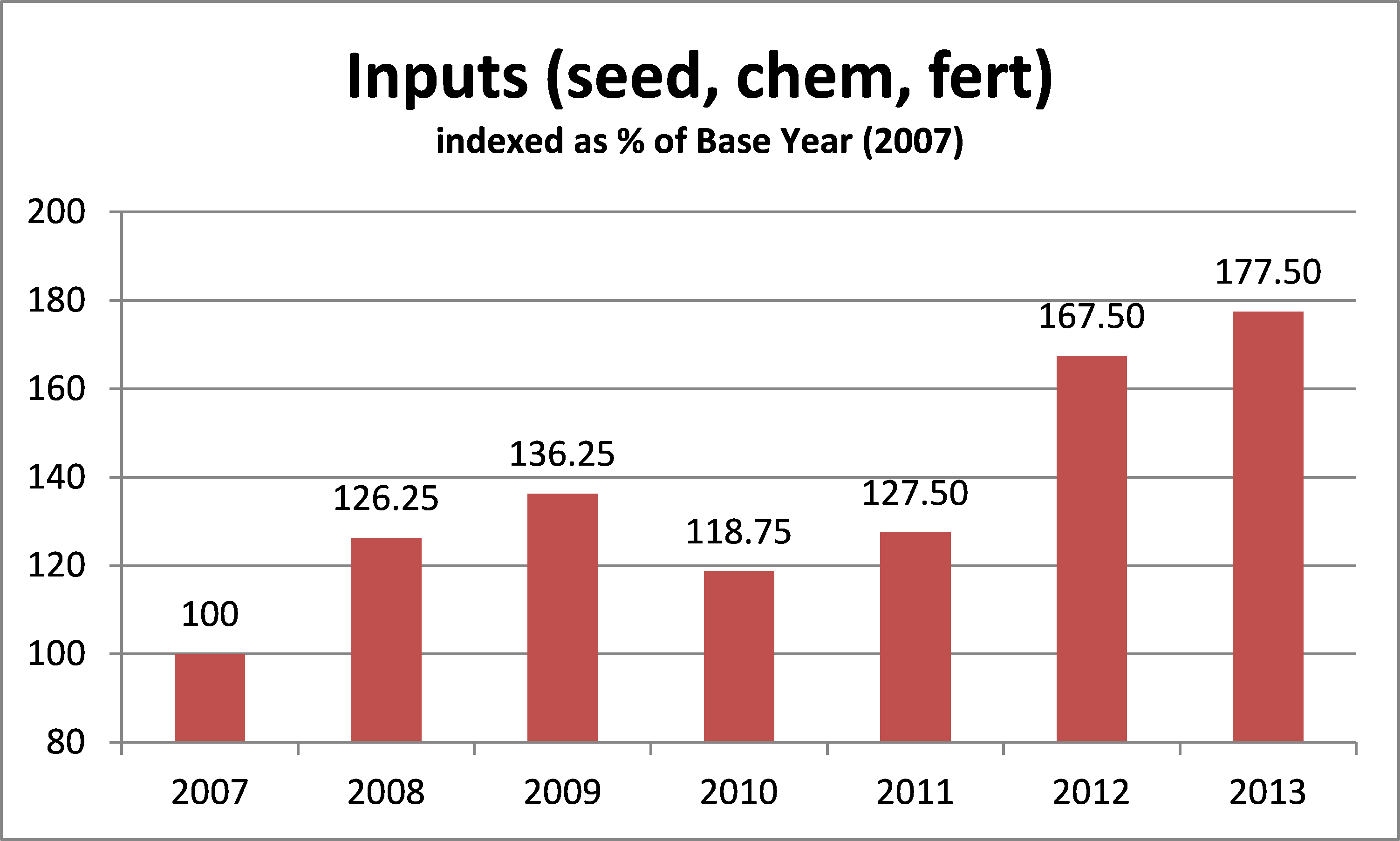

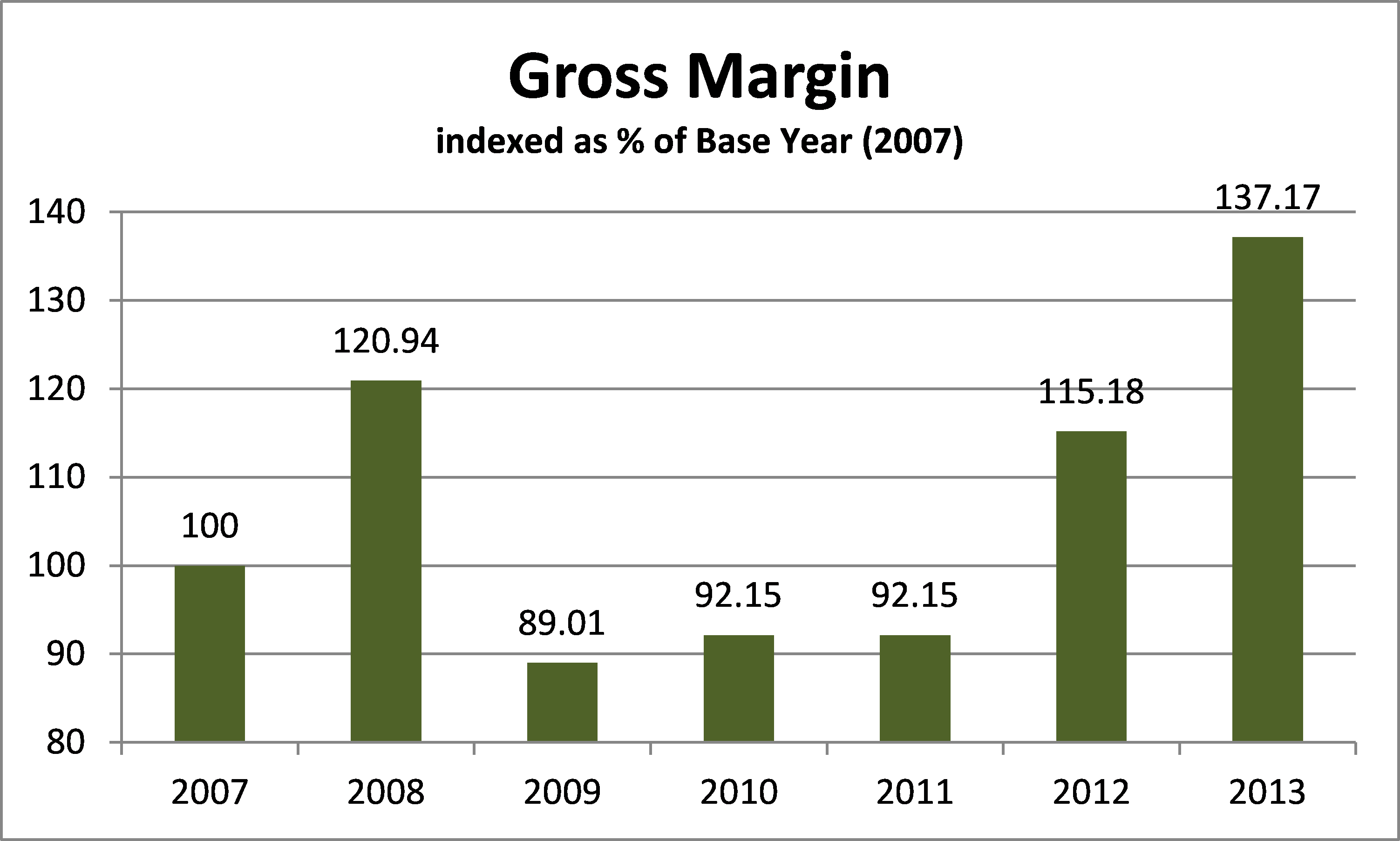

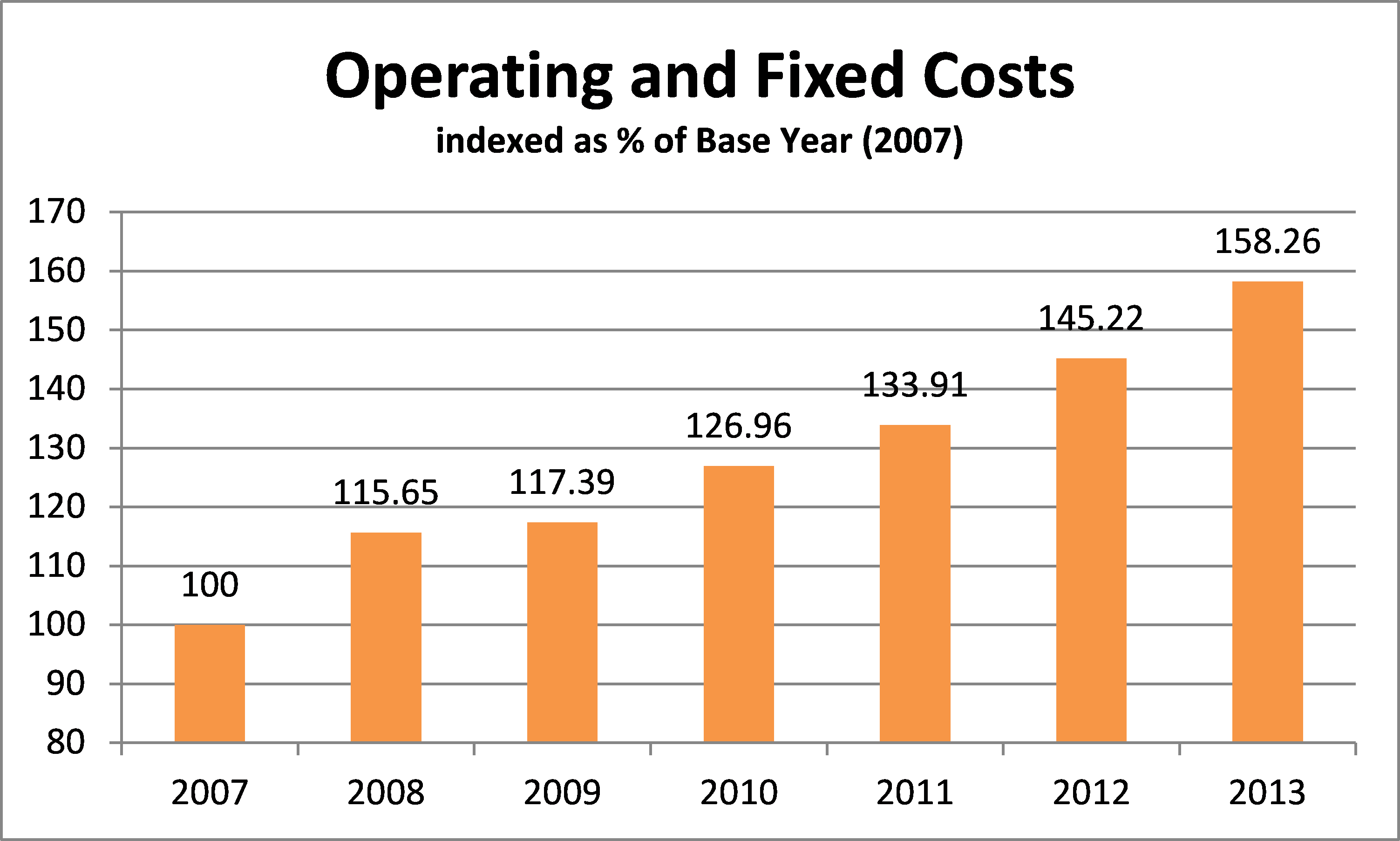

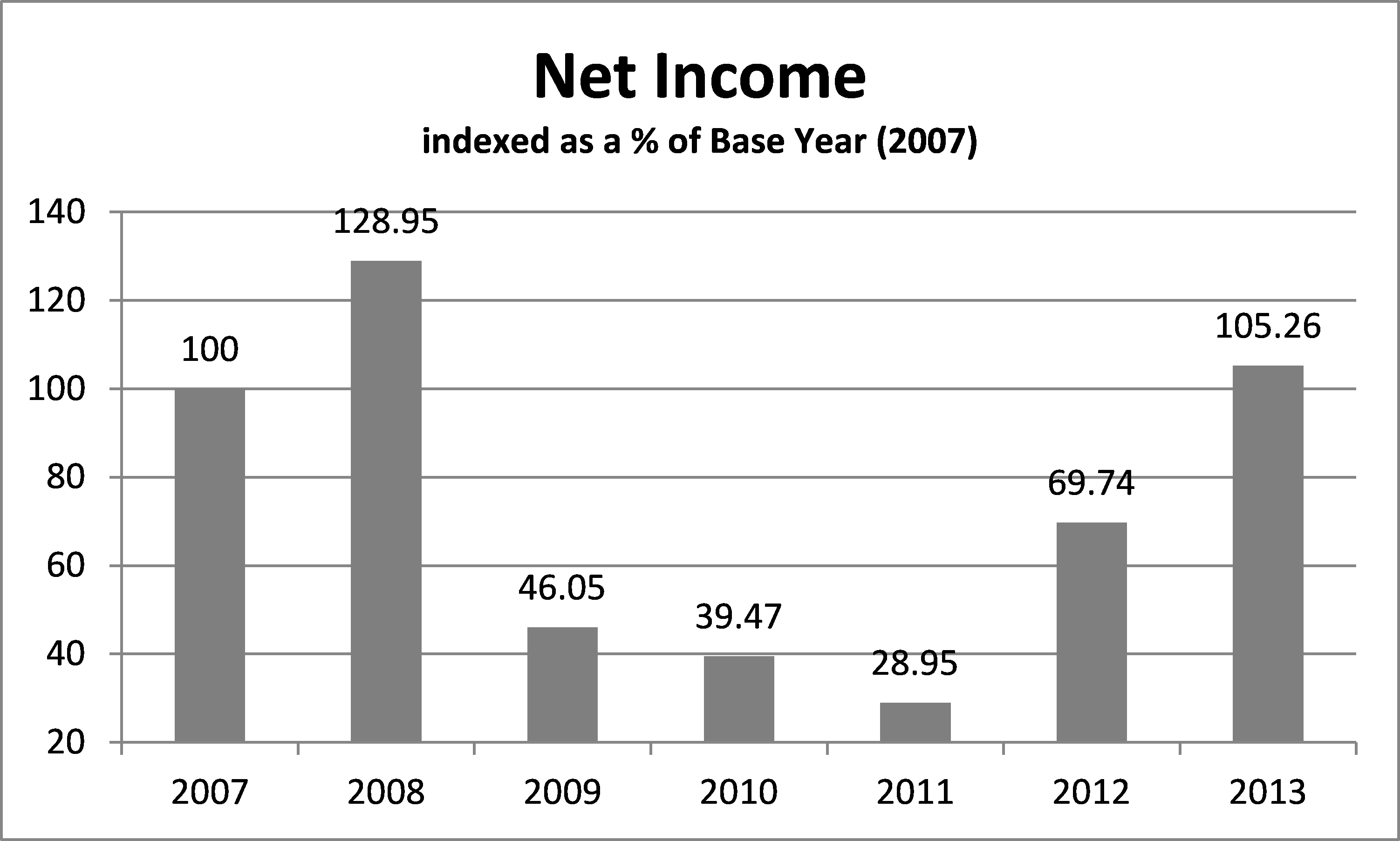

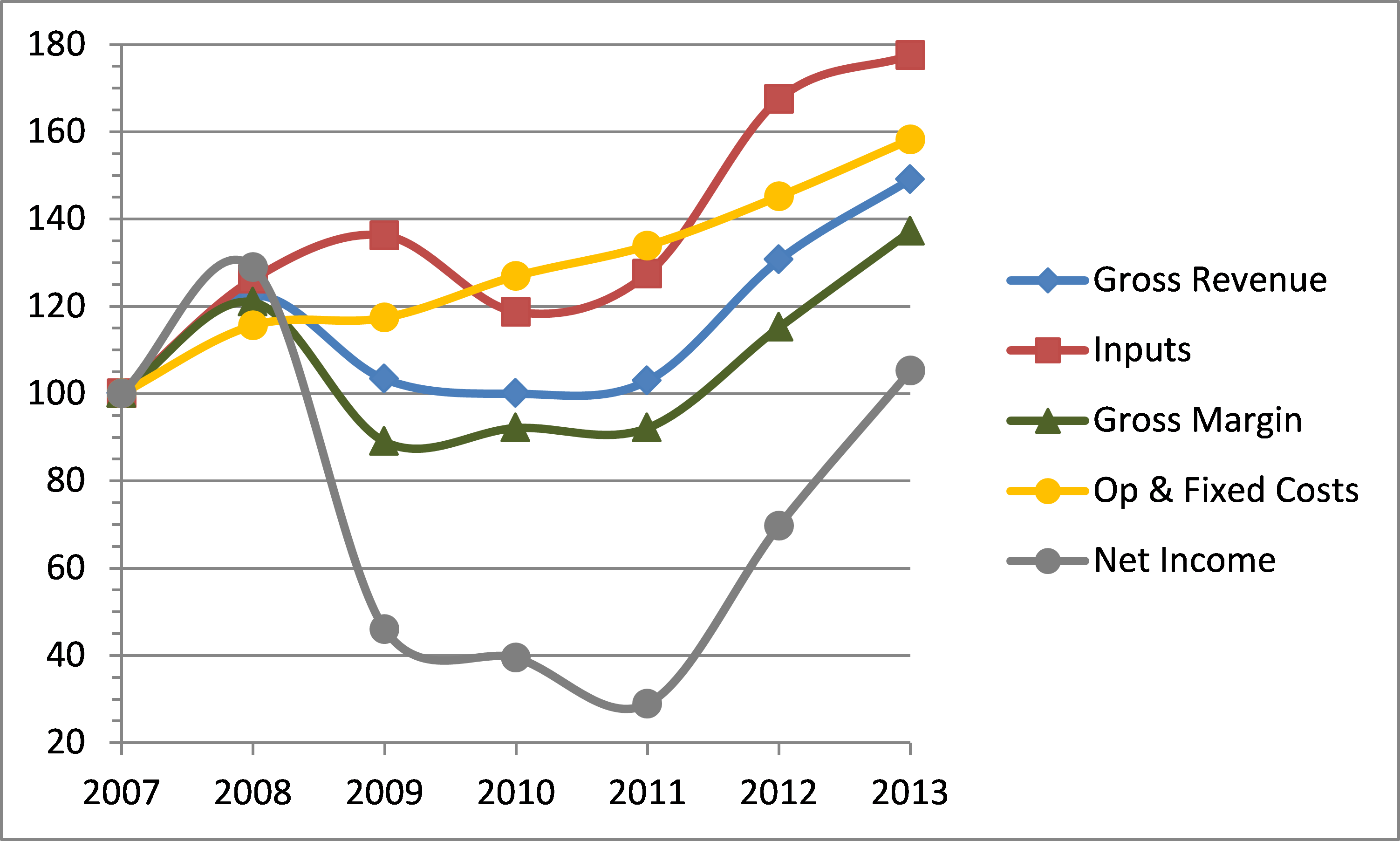

It amazes me how what was ingrained into our long term memory for so long was so quickly forgotten. The memories of the indescribable hardships of the 1980s and 1990s have seemingly been overtaken by the boom years of 2007-2013. The willingness to replace the history lessons of tight margins and poor cash flow with the euphoria of big profits and cash to burn has led to many farms now facing a debt and cash crisis similar to what was common in the final 20 years of the last century.

The trickle-down effect of debt stems from when debt levels increase as fast as, or faster than, the borrower’s long term cash flow and net income. While asset levels increase, sometimes very rapidly, tremendous growth in debt levels eat away at potential equity and use up available cash flow. While the land base has expanded and late model equipment efficiently farms all the acres, while the bins may be full and the employees are busy, it all trickles down to cash.

When the demands on your cash are a raging river, it is pretty hard to live on a trickle.