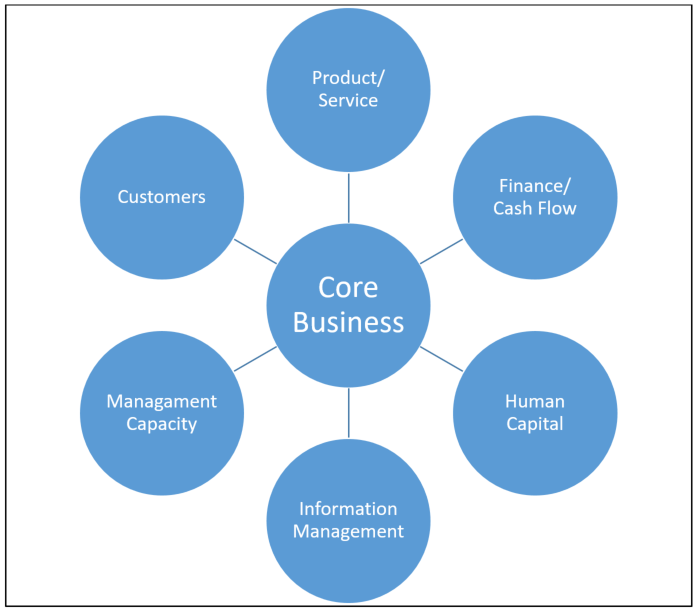

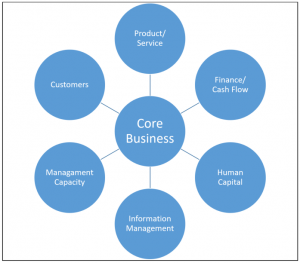

In this final installment of our discussion on the multifaceted growth opportunities that exist in your business, we will touch on Information Management and Management Capacity. One more time, here is another look at the graphic that has laid out the basis of our conversation.

Information Management

Information Management

This refers to the information that you need to run your business day to day, month to month, year to year, production cycle to production cycle, project start to project end, etc. Whatever the scope and duration required for your specific business is subjective and will be determined by you and the needs of your business. Have you given much thought to the type of information you need, what form you need it in, and how often you need it? Far too many businesses have not given this question sufficient thought.

How does a business make important decisions without sufficient information? Has your lender ever granted you new or additional credit without sufficient information? Of course they haven’t! Doing so increases risk, and banks are exceptional at managing risk.

Depending on your business and the industry in which you operate, the information you deem most critical will be different from others. For example, a business in the service industry may need to track client contacts per employee per day whereas a business in the construction industry may want to track re-work (work that needs to be redone because it wasn’t right the first time.) Critical information that is industry agnostic would include current and accurate information on liquidity, productivity, and profitability.

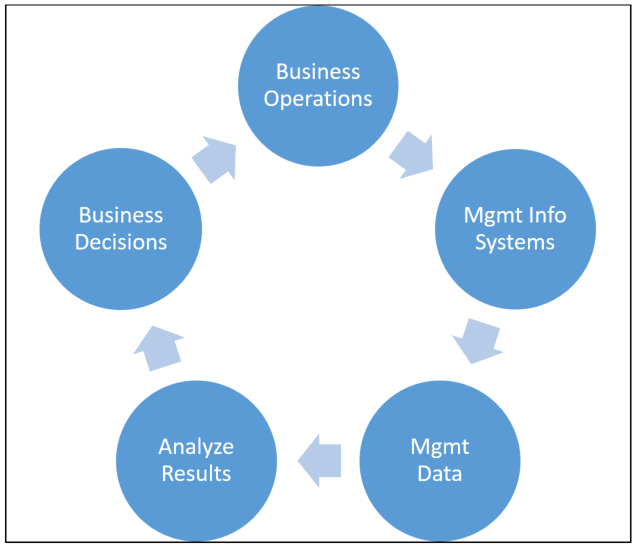

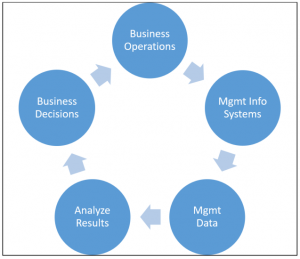

What systems do you currently use to compile your business information? Remember, systems do what they were designed to do, so if your system is not providing you with the results you want then there is a flaw in your system! Taking a look at the graphic below, your management information system(s) should collect raw data from business operations (whatever business, whatever  industry) and produce the data into a useful form, typically a report of your preference, so that management can analyze the results of what has happened in your business over the last period of time (week, month, quarter, etc.) Business decisions get made which affect operations, and those decisions get made anyway, even if out of necessity. So why not make informed decisions that are impactful, progressive, and positive?

industry) and produce the data into a useful form, typically a report of your preference, so that management can analyze the results of what has happened in your business over the last period of time (week, month, quarter, etc.) Business decisions get made which affect operations, and those decisions get made anyway, even if out of necessity. So why not make informed decisions that are impactful, progressive, and positive?

If working capital is tight, would it be helpful to learn that your customers take 3 weeks longer to pay that you thought? If profitability is not meeting expectations, would it help to know that profit margins have been shrinking? If productivity is under budget, would it help to know that employee sick days have been on the rise? What you think are problems in your business (tight working capital, shrinking profit margins, decreased productivity) are actually symptoms of the real problem (which in this case could be lengthy accounts receivable, poor inventory control, or lack of staff morale…)

If you are going to step up from trying to treat the symptom by first learning what actually is the problem, then you need good management information.

Management Capacity

Coming from the farm and having spent most of my professional career working in agriculture, I often get asked a specific question by people who grew up on farms in the ’50s or ’60s but have left the farm as young adults and never got involved in farming. They ask, “These farms are getting bigger and bigger; how big is too big?” My response is, “I can tell you exactly when. It’s when the farm has expanded beyond the owner’s/manager’s ability to manage it! For some, that is 40,000 acres; for others, it’s 400 acres.”

**NB: Not looking at corporate city limits but actual development, 40,000 acres is slightly less than the size of Regina, Saskatchewan. In contrast, 400 acres is approximately the area used by the Tor Hill Golf Course.

Business owners/managers (these roles are not synonymous, by the way) must be proficient in many different aspects of their business. One might say that business owners “need to wear many hats.” Being an expert in the work your business does is important, but if that is where your capacity ends, then you surely have “fallen prey to The Fatal Assumption” that Michael Gerber wrote about in The E-Myth Revisited. Just to name a few, strategist, controller, marketer, recruiter, trainer, collector, innovator, and leader are but a smattering of the hats a business owner must wear at some point or another. If your capacity while wearing any of those hats is less than “expert”, then you might be inhibiting growth!

Business owners/managers (these roles are not synonymous, by the way) must be proficient in many different aspects of their business. One might say that business owners “need to wear many hats.” Being an expert in the work your business does is important, but if that is where your capacity ends, then you surely have “fallen prey to The Fatal Assumption” that Michael Gerber wrote about in The E-Myth Revisited. Just to name a few, strategist, controller, marketer, recruiter, trainer, collector, innovator, and leader are but a smattering of the hats a business owner must wear at some point or another. If your capacity while wearing any of those hats is less than “expert”, then you might be inhibiting growth!

“Do what you do best, and get help for the rest™” is a cornerstone of my advisory work with clients, and as such, I’ve trademarked it. If we spent our entire lives trying to improve on our weaknesses, we would reach the end of our lives with a bunch of strong weaknesses. However, if we spend our lives utilizing our strengths and utilizing the strengths of others in areas we are weak, then we create a synergy that provides incredible leverage not only for our business, but for ourselves and the people we have hired!

Take a moment this week to perform a self-audit on where your capacity is reaching its limit. Growth is about breaking through limitations, and this becomes an exceptional opportunity for growth, both in your person and in your business.

Plan for Prosperity

Growth is about more than just size and scale, but it is about expanding. Growth is expanding our view, our skills, and our attitudes. Growth is about expanding our network, our credibility, and our place in the market. We’ve just completed a three-part journey that coursed through the many facets of growth. In summary:

- Your customers give your business a reason for being. How do you find them and keep them?

- Your product or service can be your boom or bust. Are you innovating how your deliver your product/service? Where is your link in the value chain?

- Pursuing growth from a position of financial weakness is a recipe for disaster. Are your finances putting in the position for growth, or are they hindering growth opportunities?

- How are you investing in your people? Are they being trained? Are they provided with increasing responsibility? What type of culture does your business have?

- Accuracy of your management information is critical. Is your information system up to par? Are you making critical decisions with outdated or inaccurate information?

- If you are the heart and soul of your business, is your capacity in any of the critical management functions you perform a limiting factor in your business’ growth?

You business is like a tree: if it is not growing, it is dying. But unlike a tree, your business has many ways it can grow. Always grow, and grow all ways.