It Can’t Happen to Me

Have you heard?

Things aren’t all roses in agriculture lately. Sure there are some who are doing quite well, and of course the recent drought gets the credit for any 2017 results that were sub-par, but what about those who still did okay during the drought? What about those who are still sub-par when everything is firing on all cylinders?

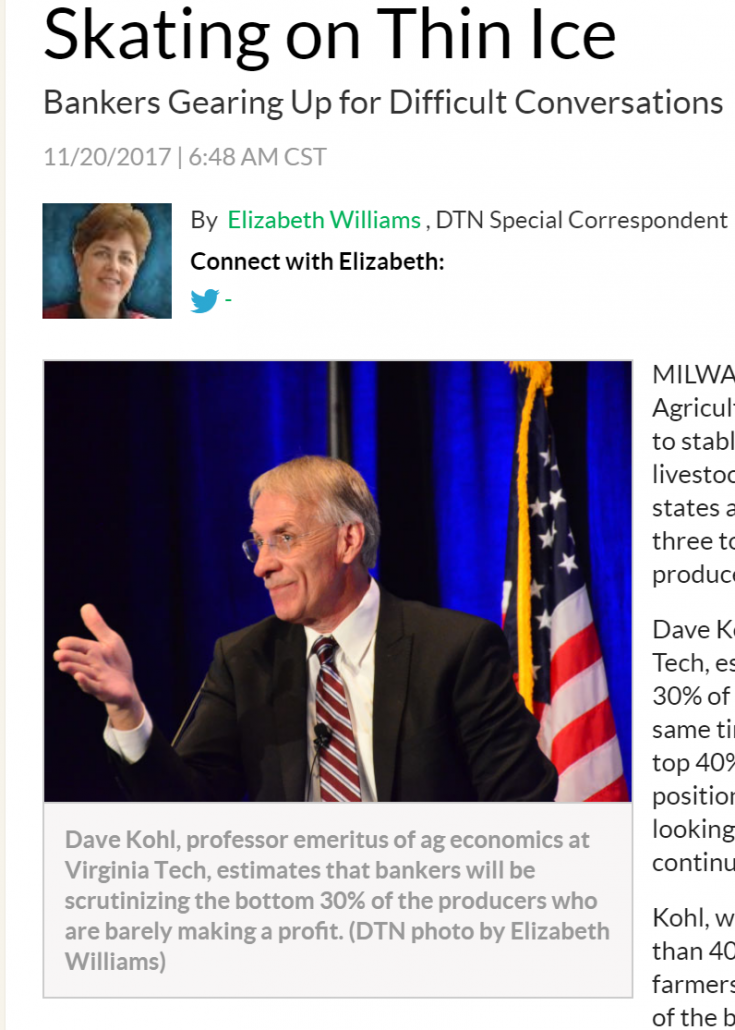

A recent article on DTN titled Skating on Thin Ice summarizes the message of Dr. David Kohl, renowned ag economist, at the National Agricultural Bankers Conference earlier this month. Dr. Kohl has been advising ag bankers for over 40 years. He’s got some chops.

His prediction (in summary): there will be clear winners and losers, the losers being the bottom 30% of all producers.

What makes the bottom 30%? They barely make a profit, have burnt through most (or all) of their working capital, and are beginning to burn through their equity. Dr. Kohl suggests that a farm in this position consider exiting before all equity is gone.

It was back in 2016, over a year ago now, that rumblings were coming out of the US Mid-West about farm lenders tightening up on credit approval criteria. I tweeted the following:

Dear #westcdnag

Does anyone think this can't happen here? https://t.co/LFYEMg1Cb0— Kim Gerencser (@KimGerencser) September 15, 2016

We’ve already seen an increase in interest rates from the Bank of Canada, and we are to expect more according to messages from our federal government. But do not think that your interest rate can only be changed by the BofC. Lenders set interest rates according to how your business is risk-rated. If you’ve already burnt through your working capital and have moved on to burning equity, you are considered to be high risk and will be charged interest accordingly.

Land value appreciation has propped up many farms that have a history of poor operating profits.

Remember when we talked about how the commodity super cycle (2007-2013) allowed below-average management skills to generate above-average results? (Ref. Vol.3 /No.44 Happy Halloween) Even those producers who were not able to produce a profit from operations could still show that equity levels were increasing because their land was appreciating. This created a false sense of security, and a false sense of accomplishment.

Notwithstanding what is going on in US ag lending, the landscape in Canadian ag lending can change. The bank’s desire to support businesses that cannot generate profit from operations is limited. Are you on the radar?

To Plan for Prosperity

Allowing your relationship with your lenders to be anchored by land value appreciation only, and not profit from operations, could make you a subject for a change to your borrowing terms. How would your business be affected if your interest rates increased by 1%, or if your credit limits were reduced by one-third? If your current lender views you as high risk, other lenders will too…

Leave a Reply

Want to join the discussion?Feel free to contribute!